Navigating the complexities of insurance coverage for individuals with mental illness can be challenging. Mental health conditions are often considered pre-existing conditions, which may affect the availability and cost of insurance plans. However, with the implementation of the Affordable Care Act (ACA), also known as Obamacare, many barriers to mental health coverage have been reduced. The ACA mandates that mental health services be covered as essential health benefits, making it more accessible for individuals to obtain insurance that includes mental health treatment. Despite these advancements, disparities in coverage and access to care persist, and understanding the intricacies of insurance policies remains crucial for those seeking mental health support.

Explore related products

What You'll Learn

- Types of Mental Illnesses Covered: Explore which mental health conditions are typically included in insurance plans

- Insurance Providers and Policies: Research various providers and their specific policies regarding mental health coverage

- Cost and Premiums: Analyze the financial aspects, including premiums and out-of-pocket costs associated with mental health insurance

- Network and Access to Care: Evaluate the network of mental health professionals and facilities available through different insurance plans

- Legal Protections and Rights: Understand the legal framework protecting individuals with mental illnesses in the context of insurance coverage

![]()

Types of Mental Illnesses Covered: Explore which mental health conditions are typically included in insurance plans

Insurance coverage for mental health conditions varies widely depending on the specific policy and provider. However, many standard insurance plans now include coverage for a range of mental illnesses due to increased awareness and advocacy efforts. Common conditions covered include depression, anxiety disorders, bipolar disorder, schizophrenia, and obsessive-compulsive disorder (OCD). Some plans may also cover substance abuse treatment and eating disorders.

The extent of coverage can differ significantly between plans. For instance, while some policies may offer comprehensive coverage including therapy sessions, medication, and inpatient treatment, others may have limitations on the number of therapy sessions allowed per year or may require higher copays for mental health services. It's crucial for individuals to review their policy details carefully to understand what is covered and what out-of-pocket expenses they may incur.

In addition to the specific mental health conditions covered, insurance plans may also have different requirements for pre-authorization or referrals. Some plans may require a primary care physician's referral to see a mental health specialist, while others may allow direct access to mental health services. Understanding these requirements can help individuals navigate the insurance system more effectively and ensure they receive the care they need.

When selecting an insurance plan, individuals with mental health concerns should consider the plan's mental health coverage as a key factor. This includes not only the types of conditions covered but also the network of mental health providers available, the cost of services, and any limitations or exclusions. By carefully evaluating these aspects, individuals can choose a plan that best meets their mental health needs and provides the necessary support and resources.

Navigating Legal Avenues: Can a Lawyer Secure Your Release from a Mental Hospital?

You may want to see also

Explore related products

![]()

Insurance Providers and Policies: Research various providers and their specific policies regarding mental health coverage

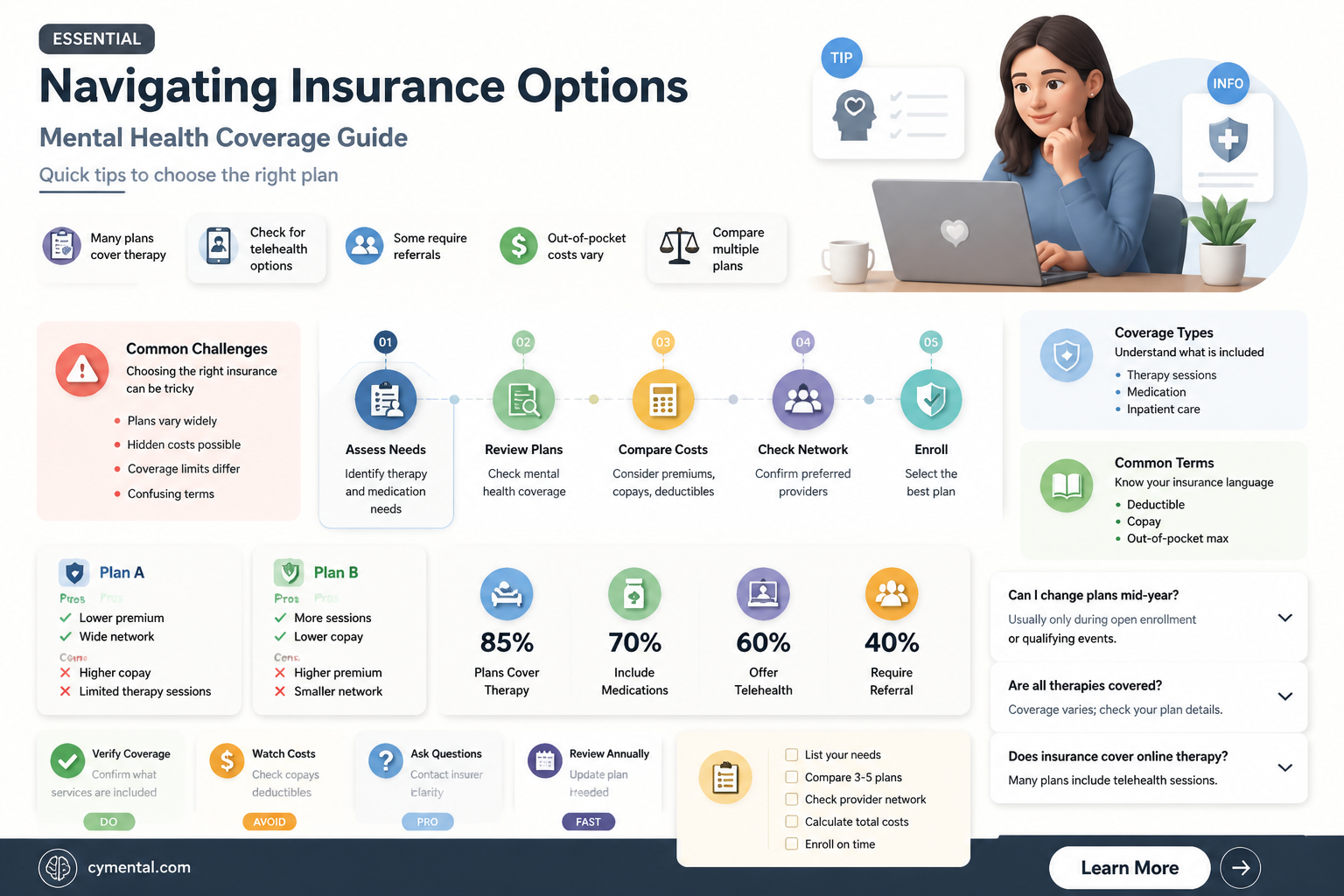

Researching various insurance providers and their specific policies regarding mental health coverage is crucial for individuals seeking appropriate insurance. Each provider may have different criteria, coverage limits, and exclusions that can significantly impact the level of care a person with a mental illness can receive. It is essential to compare policies from multiple providers to find the best fit for one's needs.

When evaluating insurance policies, it is important to consider the following factors: the types of mental health services covered (such as therapy, medication, hospitalization), the maximum number of sessions or days covered per year, the presence of any pre-existing condition clauses, and the out-of-pocket costs (deductibles, copays, coinsurance). Additionally, some policies may have specific requirements for referrals or pre-authorization for certain treatments, which can affect the ease of accessing care.

To conduct thorough research, individuals can start by obtaining quotes from multiple insurance providers and reviewing the policy documents in detail. They can also consult with insurance brokers or mental health professionals who may have experience with different providers and policies. Online resources and reviews can provide valuable insights into the experiences of others with similar needs.

It is also advisable to consider the provider's network of mental health professionals and facilities. A larger network may offer more options for care, while a smaller network could limit access to specific providers or treatments. Furthermore, individuals should be aware of any state or federal laws that may protect their rights to mental health coverage, such as the Mental Health Parity and Addiction Equity Act in the United States.

In conclusion, researching insurance providers and policies is a critical step in ensuring that individuals with mental illnesses can access the care they need. By carefully evaluating the coverage options, costs, and requirements of different policies, individuals can make informed decisions that will help them manage their mental health effectively.

Finding Support: A Guide to Resources and Assistance

You may want to see also

Explore related products

![]()

Cost and Premiums: Analyze the financial aspects, including premiums and out-of-pocket costs associated with mental health insurance

The financial aspects of mental health insurance can be complex and vary widely depending on the specific policy and provider. Premiums for mental health coverage are typically higher than those for physical health insurance due to the higher costs associated with mental health treatment. In addition to premiums, individuals may also face out-of-pocket costs such as deductibles, copays, and coinsurance. These costs can add up quickly, especially for those who require ongoing treatment or therapy.

One unique angle to consider when analyzing the financial aspects of mental health insurance is the impact of parity laws. These laws require insurance providers to cover mental health services at the same level as physical health services, which can help to reduce out-of-pocket costs for individuals seeking mental health treatment. However, parity laws do not necessarily guarantee that mental health services will be affordable, as insurance providers may still impose high premiums and out-of-pocket costs.

Another important factor to consider is the availability of subsidies and financial assistance programs. Many insurance providers offer subsidies or discounts to individuals who meet certain income or eligibility criteria. Additionally, government programs such as Medicaid and Medicare may provide mental health coverage at a lower cost than private insurance.

When evaluating the financial aspects of mental health insurance, it is also important to consider the long-term costs of untreated mental illness. While the upfront costs of insurance premiums and out-of-pocket expenses may seem high, the long-term costs of untreated mental illness can be much more significant, including lost productivity, strained relationships, and increased risk of physical health problems.

In conclusion, analyzing the financial aspects of mental health insurance requires a careful consideration of premiums, out-of-pocket costs, parity laws, subsidies, and the long-term costs of untreated mental illness. By understanding these factors, individuals can make informed decisions about their mental health coverage and seek the treatment they need without facing financial hardship.

Unraveling the Decline: Why My Mental Health Is Worsening

You may want to see also

Explore related products

![]()

Network and Access to Care: Evaluate the network of mental health professionals and facilities available through different insurance plans

Evaluating the network of mental health professionals and facilities available through different insurance plans is crucial for individuals seeking comprehensive mental health care. Insurance plans vary significantly in their coverage, and understanding the nuances can make a substantial difference in the quality of care one receives. For instance, some plans may have a robust network of psychiatrists and therapists, while others might offer limited options, potentially impacting the continuity and effectiveness of treatment.

When assessing an insurance plan's network, it's essential to consider the types of mental health professionals included, such as psychiatrists, psychologists, licensed therapists, and social workers. Additionally, the availability of specialized facilities, like inpatient treatment centers or outpatient clinics, should be examined. Plans with a broader network typically provide more flexibility and better access to a range of services, which can be particularly important for individuals with complex or severe mental health conditions.

Another critical aspect to evaluate is the plan's coverage for telehealth services. With the increasing adoption of telemedicine, having access to virtual mental health appointments can be highly beneficial, especially for those in remote areas or with mobility issues. Plans that include telehealth options may offer greater convenience and accessibility, potentially leading to improved engagement with mental health care.

It's also important to scrutinize the plan's policies regarding referrals and prior authorizations. Some plans may require referrals from primary care physicians or impose restrictions on the number of therapy sessions covered, which can create barriers to accessing necessary care. Understanding these limitations upfront can help individuals make informed decisions about their insurance options.

Lastly, considering the plan's customer service and support resources can provide valuable insights into the overall experience of using the insurance for mental health care. Plans with responsive customer service and robust support systems may be better equipped to handle the unique needs and challenges of mental health treatment.

In conclusion, evaluating the network and access to care offered by different insurance plans is a critical step in ensuring that individuals with mental illness can receive the comprehensive and effective treatment they need. By carefully considering the types of professionals, facilities, telehealth options, referral policies, and customer support available, individuals can make informed choices that significantly impact their mental health outcomes.

Love Beyond Walls: Marriage Possibilities in Mental Health Facilities

You may want to see also

Explore related products

![]()

Legal Protections and Rights: Understand the legal framework protecting individuals with mental illnesses in the context of insurance coverage

Individuals with mental illnesses are protected under various legal frameworks that ensure they receive fair treatment in the context of insurance coverage. One of the key pieces of legislation in the United States is the Mental Health Parity and Addiction Equity Act (MHPAEA) of 2008. This act requires insurance plans to provide coverage for mental health and substance use disorder services at a level that is comparable to medical/surgical benefits. This means that insurance companies cannot impose more restrictive limits on mental health coverage than they do on other types of medical coverage.

Another important legal protection is the Americans with Disabilities Act (ADA), which prohibits discrimination against individuals with disabilities, including mental illnesses, in various areas, including employment and public accommodations. While the ADA does not directly address insurance coverage, it does provide a broader legal framework that supports the rights of individuals with mental illnesses to access necessary services and accommodations.

In addition to federal laws, many states have their own laws and regulations that provide additional protections for individuals with mental illnesses. For example, some states have laws that require insurance companies to cover certain mental health services or that prohibit discrimination against individuals with mental illnesses in the provision of insurance.

Understanding these legal protections is crucial for individuals with mental illnesses and their families, as it can help them navigate the complex landscape of insurance coverage and ensure they receive the services they need. It is also important for healthcare providers and insurance companies to be aware of these laws to ensure they are providing appropriate coverage and services.

In conclusion, the legal framework protecting individuals with mental illnesses in the context of insurance coverage is multifaceted and includes federal and state laws that provide important safeguards against discrimination and ensure access to necessary services. By understanding these protections, individuals can better advocate for themselves and ensure they receive the coverage they are entitled to under the law.

Liberating Yourself: A Guide to Overcoming Mental Pain

You may want to see also

Frequently asked questions

Yes, a person with a mental illness can get insurance. The Affordable Care Act (ACA) prohibits insurance companies from denying coverage based on pre-existing conditions, including mental illnesses.

Yes, most insurance plans cover mental health treatment to some extent. The ACA requires that mental health services be covered at the same level as physical health services. However, the specifics of coverage can vary depending on the insurance plan.

To find insurance that covers mental health treatment, you can start by researching different insurance providers and plans in your area. You can also consult with a mental health professional or a healthcare navigator to help you understand your options and choose a plan that meets your needs.